The Board Is Set — North America Inside the Year the World Stopped Waiting

Morning Affairs · Sunday May 17, 2026 · by NA77

The week ended with Vladimir Putin en route to Beijing, hours after Trump left. In between: an Iran war cascading into global food systems, a Mexican governor indicted for cartel collusion, a $690 billion AI infrastructure sprint that North America could either lead or watch, and a $39 trillion US debt that has already crossed its World War II peak. This is not a crisis moment. This is the new architecture.

“The world is not in chaos. It is in reorganization. The difference matters — because reorganization can be navigated, and North America has assets the rest of the world cannot easily replicate. The question is whether we see them clearly enough to use them.”

THE SIGNAL

1 — The Tehran Calculation

War & Supply Chain · Britannica · FAO · WFP · Atlantic Council

On February 28, the United States and Israel launched joint strikes on Iran. The official rationale was Tehran’s nuclear program. The actual calculation was larger: control of the Persian Gulf, suppression of a proxy-warfare infrastructure spanning Lebanon to Yemen, and the assertion — at a moment of Russian and Chinese ascent — that the United States still retains the will and capacity to strike a sovereign state that crosses its thresholds.

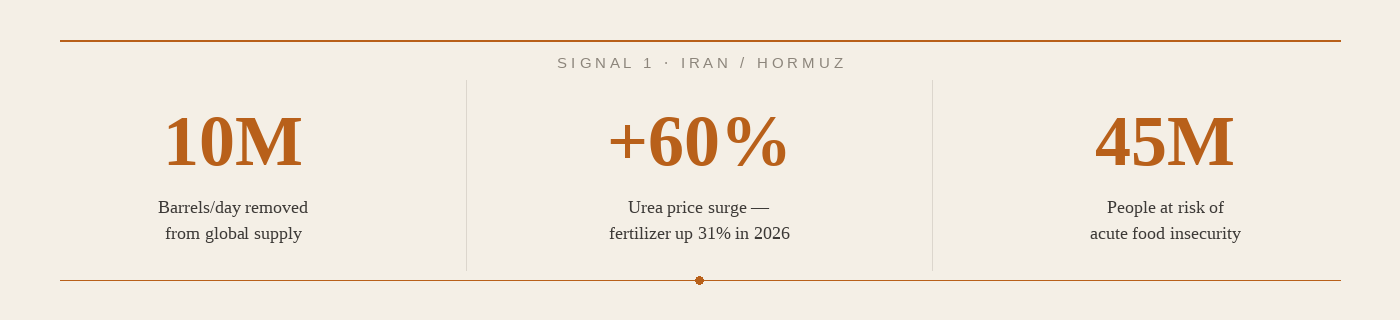

Three months on, the secondary effects are the story. The Strait of Hormuz — through which 35 percent of global seaborne crude oil and one-third of global fertilizer trade moves — has been effectively closed. An estimated 10 million barrels per day have been removed from global supply. Oil trades above $100. Urea prices are up 60 percent; fertilizer broadly projected to rise 31 percent across 2026. The FAO has warned of harvest shortfalls. The World Food Programme estimates 45 million additional people could enter acute food insecurity before year’s end.

Healthcare facilities across Lebanon, Iran, and Israel have been struck once every six hours. Water infrastructure is under attack. Over 220,000 Indian nationals have been repatriated from the Gulf. Dubai’s hotel occupancy has collapsed. The war in Iran is not a Middle Eastern story. It is a planetary supply-chain event — and it is not over.

Why it matters for North America: Fertilizer price shocks hit agricultural states from Iowa to Sonora. Energy input costs are embedding across every manufacturing corridor. The continent’s food production advantage — the ability to feed itself and export — becomes a strategic asset in a world where Hormuz is not reliably open. That advantage is only as strong as the infrastructure and the policy alignment protecting it.

2 — The Beijing Sequence

Geopolitics · CNBC · Al Jazeera · CNN · PBS · Washington Post

Trump arrived in Beijing on May 13 — the first American president to visit China in nearly a decade. He brought the CEOs of Tesla, Apple, BlackRock, and Boeing. He left two days later with trade framework agreements, a warning from Xi Jinping that mishandling Taiwan would place the relationship “in great jeopardy,” and no shared understanding of what had actually been agreed. Both governments immediately claimed different outcomes from the same conversations.

Then, less than 24 hours after Air Force One departed, the Kremlin announced that Vladimir Putin would arrive in Beijing on May 19 for a two-day visit — timed to the 25th anniversary of the Sino-Russian Treaty of Friendship. Xi Jinping received the leader of the world’s largest economy and the leader of its most sanctioned major power within the same week, letting each observe the other’s visit from a diplomatic distance of 48 hours. A joint statement will be signed. Other documents will follow.

This is not coincidence. This is architecture. Beijing is signaling, with the precision of a calendar, that it alone sits at the center of both conversations simultaneously — as indispensable partner to Washington and as strategic anchor for Moscow. China does not need to choose. It has positioned itself so that others must choose while it holds the center.

The G2 question. Trump’s visit has revived serious discussion of a US-China bilateral condominium — a “G2” in which the two largest economies manage global affairs together, structurally sidelining Europe, Japan, and the rest. If that architecture hardens even informally, North America’s bilateral relationships with Washington become more transactional, and the value of a genuinely integrated continental bloc — not three nations each managing a Washington relationship separately — becomes the only answer that doesn’t leave Canada and Mexico permanently outweighed.

Why it matters: North America was not in the room in Beijing. Canada and Mexico were not at the table where trade frameworks, rare earth access, Taiwan redlines, and AI cooperation parameters were being negotiated. The continent’s three nations each manage their Washington relationships separately — which means the combined weight of the continent was absent from the most consequential diplomatic week of 2026 so far.

3 — Taiwan: The Fault Line That Does Not Need an Invasion to Move

Security · Foreign Policy · The Diplomat · AEI · Al Jazeera

China is not, by most serious assessments, prepared to invade Taiwan in 2026. But the trajectory has shifted in ways that do not require invasion to become catastrophic. Japanese Prime Minister Takaichi’s statement — that Japan could defend Taiwan if attacked — forced Beijing to revise its military planning assumptions for the first time in years. Japan has since transited the Taiwan Strait with a destroyer and is deploying missile systems to Yonaguni island, 110 kilometers from Taiwan’s coast. China has responded by tightening rare earth exports and escalating naval pressure near Japanese waters.

Both sides believe they are deterring the other. That is the pattern that tends to develop its own logic — and its own accidents. Xi’s warning to Trump was not rhetorical. After the summit, it has been formalized. The absence of an invasion is not the same as stability. What is building is a permanent military readiness posture in which the probability of unintended escalation rises with every additional deployment.

The North American connection is direct. China’s rare earth export tightening — the weapon deployed in response to Japan’s posture — is the same lever that cuts semiconductor supply chains running from TSMC to factories in Michigan, Monterrey, and Ontario. Taiwan is not an abstraction for the continent’s industrial system. It is where the chips are made.

Why it matters: Canada’s minerals and Mexico’s manufacturing matter for AI and semiconductor supply chains precisely because Taiwan’s security cannot be assumed. A North American continental minerals strategy — from Canadian cobalt and lithium to Mexican assembly capacity — is not idealism. It is the supply chain insurance the continent needs if the Taiwan Strait situation deteriorates further.

4 — Sinaloa: The Rot Inside the Room, and What It Means for July 1

Rule of Law · USMCA · Al Jazeera · CSIS · InSight Crime · NBC News

On April 29, a New York federal court unsealed an indictment charging Sinaloa Governor Rubén Rocha Moya and nine other current and former Mexican officials with conspiracy to traffic narcotics into the United States. The allegations are specific: members of the Sinaloa Cartel’s Chapitos faction allegedly helped secure Rocha Moya’s 2021 election — kidnapping opposition candidates, stealing ballot papers — in exchange for his pledge to let the cartel operate with impunity. A sitting senator and the mayor of Culiacán were also charged. All are Morena. On May 15, the former Sinaloa security chief was arrested in the United States on related charges.

Rocha Moya resigned temporarily on May 2, denying all charges. President Sheinbaum defended sovereignty: Mexico will try its own officials in its own courts. There will be no extradition. The indictments are not purely a law enforcement act. They are a diplomatic instrument — timed, calibrated, and placed on the table precisely as the USMCA review approaches its most consequential moment.

July 1 is the formal USMCA decision node — the date by which the three parties must signal whether to extend, renegotiate, or trigger withdrawal procedures. The US has made explicit that security cooperation and trade access are now linked. Indicting a Morena governor, senator, and mayor places Sheinbaum in an impossible position. Act against her own coalition’s officials and acknowledge the state penetration Washington is describing — or defend sovereignty and signal to US negotiators that Mexico cannot be a reliable security partner. Either path complicates USMCA in ways no trade text captures.

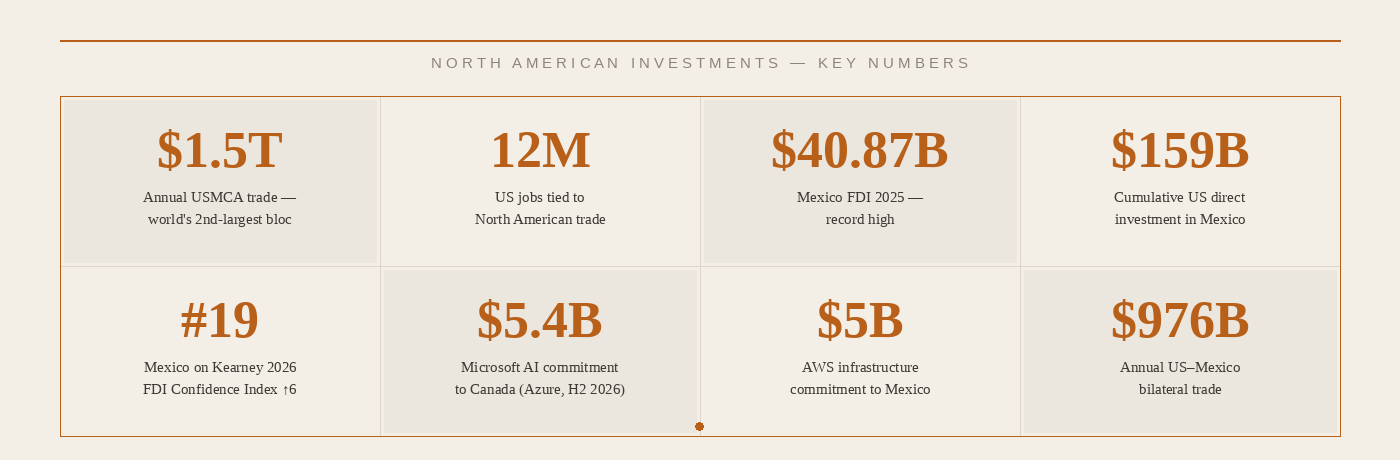

For the foreign investment thesis: every CEO making a capital allocation decision about the Mexican corridor now carries this question. The $40.87 billion in FDI Mexico attracted in 2025 is a bet the country had to perform on. The Rocha Moya indictment is the most public evidence yet of how wide the gap between geographic advantage and institutional capacity remains.

The Morena paradox. Morena was built as a movement of national dignity — against the elite networks that governed Mexico through institutional corruption. That identity now faces its most serious internal contradiction: if the governing coalition contains officials whose collaboration with designated terrorist organizations is a matter of U.S. federal record, the sovereignty narrative fractures from the inside. This is not an external attack on Morena. It is a mirror.

Why it matters: The chess piece has been placed on the board with precision. The clock is running toward July 1. Operators building in the corridor need scenario plans for both a strengthened and a degraded USMCA framework — because Sheinbaum’s response to the indictments, not the formal negotiating text, is the leading indicator of which scenario materializes.

5 — The $690 Billion Sprint: What It Demands from North America, and What North America Can Offer

AI · Investment · Futurum · Kalkine · Mexico Business News · Canadian Mining Journal · CNBC

The five largest US cloud and AI infrastructure providers — Amazon, Google, Meta, Microsoft, and Oracle — have collectively committed between $660 billion and $725 billion in capital expenditure for 2026. Roughly 75 percent of that spend, approximately $500 billion, is directly tied to AI infrastructure: servers, GPUs, data centers, and the energy systems to power them. This is not a technology investment cycle. It is an infrastructure build of the kind that, historically, reshapes geographies and labor markets for decades. The last comparable moment was the electrification of the American continent in the early twentieth century. What that moment demanded — copper, land, energy, skilled labor, logistics corridors — this moment demands again, in different form but identical logic.

The critical constraint is not capital. It is the physical inputs: land with power access, clean and reliable energy, the critical minerals that build the chips, and the manufacturing capacity to assemble and deploy at scale. On every one of these dimensions, North America — as a continental system — holds structural advantages that no other region can easily replicate. The question is whether the three nations see those advantages as a shared system, or continue to manage them as three competing national inventories.

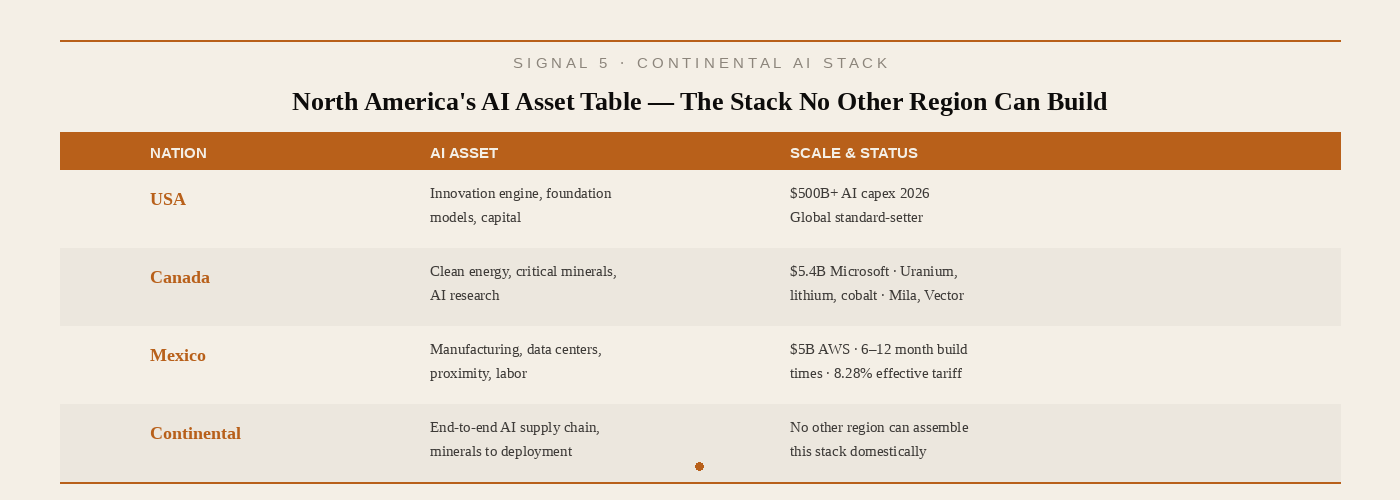

What the US brings: The innovation engine. The world’s most capable AI research base, concentrated in California, New York, and increasingly in the corridor between Chicago and Houston. The largest pool of AI capital and the deepest foundation model capabilities on the planet. The regulatory and market scale that sets global standards. No other nation is close.

What Canada brings — and why it matters now: Canada is the continent’s quiet AI superpower, and it is beginning to understand that. The country holds world-class AI research institutions in Montreal (Mila, the institute behind many of the foundational breakthroughs in deep learning), Toronto (Vector Institute), and Vancouver. Microsoft committed CAD 7.5 billion — approximately US $5.4 billion — to expand its Azure Canada regions, with capacity online by late 2026 as part of a broader $19 billion commitment to Canadian digital infrastructure through 2027.

But Canada’s deeper contribution is physical. The country possesses critical minerals — cobalt, lithium, nickel, uranium, rare earths — at a scale and with a geopolitical security profile that China and Central Asia cannot match. British Columbia has commissioned North America’s first dedicated lithium refining plant. The Canadian Photonics Fabrication Centre in Ottawa is North America’s only public compound semiconductor foundry. Canada’s clean energy infrastructure — hydroelectric power in Quebec, nuclear in Ontario — provides the stable, low-carbon electricity that hyperscale data centers require and that power-constrained markets in Northern Virginia and Silicon Valley can no longer reliably deliver.

Canada’s April uranium export halt — which produced an immediate 41% price spike — was not only a trade negotiation instrument. It was a demonstration that Canada holds irreplaceable inputs to the AI and energy system that the United States is betting its technological future on. That leverage exists. The question is whether Canada uses it strategically or defensively.

What Mexico brings — and why the window is open now: Mexico is becoming Latin America’s leading AI data center investment hub, and the numbers reflect the structural logic. AWS committed $5 billion to Mexican infrastructure — the largest single technology infrastructure outlay in Latin American history. Google launched a dedicated Mexico cloud region. The AI data center market in Mexico was valued at $70 million in 2025 and is projected to grow to $261.5 million by 2031, at a compound annual growth rate of 24.55 percent.

The competitive advantage is specific and defensible. New data centers in Mexico’s emerging hubs — Querétaro, Nuevo León, Jalisco, and Sonora — complete construction in 6 to 12 months. Equivalent builds in Northern Virginia and Silicon Valley now require 18 to 24 months. Mexico’s geographic proximity to US demand centers means latency advantages that matter for real-time AI inference workloads. Mexico operates at approximately 8.28 percent effective US tariff rate versus 39 percent for Chinese goods. That differential is the structural case for the AI manufacturing corridor.

US data center electricity demand will rise from 147 terawatt-hours in 2023 to 606 terawatt-hours by 2030 — nearly 12 percent of total US power demand. That energy has to come from somewhere. Canada’s clean hydroelectric and nuclear capacity is the most scalable, lowest-carbon, most geopolitically secure answer on the continent. The chips that run those data centers require cobalt, lithium, nickel, and rare earth elements that Canada and — through USMCA-aligned frameworks — Mexico can supply without the strategic dependence on Chinese processing that currently makes every Western AI player vulnerable. Together, these three nations possess every element of a complete AI supply chain — from the ground to the data center to the model. No other region on Earth can say the same.

The risk the continent must name. Mexico’s water scarcity — especially in northern industrial corridors — is a direct constraint on data center buildout, which requires vast cooling capacity. CFE’s energy reliability gaps create operational risk for facilities that require 99.999% uptime. The rule of law environment, now in sharper focus after the Rocha Moya indictments, introduces compliance complexity for hyperscalers with global regulatory exposure. Canada’s risk is different: political friction with Washington during the USMCA review, combined with an instinct toward resource nationalism, could convert its supply leverage from an asset into an obstacle. And across all three nations: there is no shared continental AI industrial strategy. China is deploying one. North America is not. That asymmetry is the defining strategic risk of this moment.

Why it matters: The $690 billion being deployed this year is not waiting for USMCA to resolve. It is making decisions now — where to build, which minerals to lock in, which energy contracts to sign. North America has a narrow window in which its combined assets can be positioned as a continental offer, not three competing national bids. The continent that assembles this stack coherently will not just participate in the AI economy. It will anchor it.

6 — The Supply Chain Stakes: Billions of Lives Inside Systems Nobody Named

Supply Chain · FAO · IEA · Fast Company · Tech Policy Press

The systems that feed, fuel, and connect the global economy were built on one foundational assumption: that no major power would deliberately sever the infrastructure on which all powers depended. That assumption is breaking. The Hormuz closure is not a scenario in an analyst’s model — it is the passage through which the fertilizer that grows food on four continents moves every month. The rare earths China is now weaponizing supply the semiconductors running factories in Michigan, Monterrey, and Ontario. The undersea cables carrying financial data pass near conflict zones that did not appear on most risk maps a decade ago.

Billions of people do not observe these systems from a distance. They live inside them. The disruption is already arriving — in grocery prices, in harvest shortfalls projected for late 2026, in shipping routes redesigned around a strait that was not supposed to close. North America’s geographic advantage — a continent that can feed itself, power itself, and manufacture within its own borders — is not a luxury in this environment. It is the most defensible strategic position on the planet. The continent simply has not organized itself to use it.

Why it matters: The decade ahead will be defined by supply chain sovereignty. Nations and regions that secured their mineral inputs, energy systems, food production, and manufacturing capacity before the next disruption will set the terms of global commerce. The USMCA review in July is not a trade negotiation. It is a question of whether three nations will use their combined geography as a system, or manage it separately until that option is no longer available.

7 — The Fiscal Floor, and the Global Police Problem Nobody Is Solving

Fiscal Policy · Fortune · CRFB · GAO · Hoover Institution

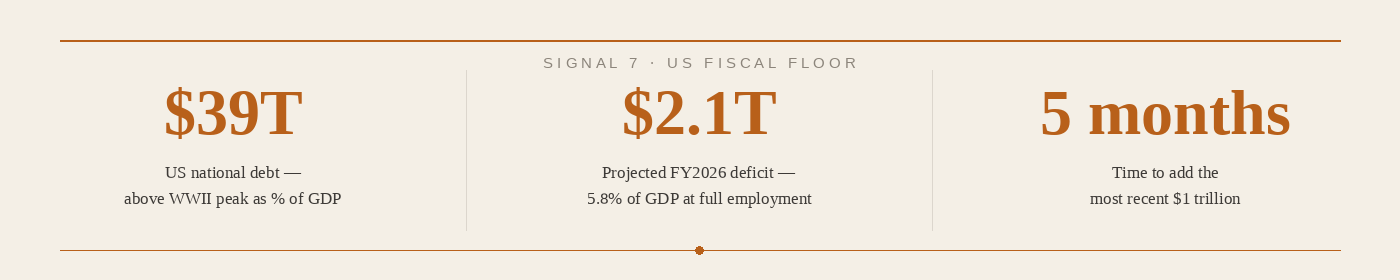

The United States entered all of this carrying $39 trillion in national debt — a ratio to GDP that crossed its own World War II peak this spring. The CBO projects the FY2026 deficit at $1.9 to $2.1 trillion: 5.8 percent of GDP, at nominal full employment. The GAO has used the word “unsustainable” in formal reports. The debt is expected to reach $40 trillion before fall 2026 — adding its most recent trillion in less than five months.

For seven decades, the United States played a specific role: architect of the international system, guarantor of global stability, the power whose predictability kept the most dangerous escalations from becoming irreversible. That role required absorbing costs that other powers would not, managing alliances through respect rather than coercion, and treating the rules-based order as an asset worth protecting even at short-term expense. That role is changing.

The Trump administration has demonstrated across multiple theaters a willingness to use American power not to maintain the system but to extract advantages from it — tariffs as leverage, indictments as diplomatic tools, military strikes as strategic assertion, summits as commerce. Allies have begun hedging. Rivals have begun probing. The spaces that American predictability used to fill are attracting new occupants. The world is not in chaos. It is in reorganization.

The US knows what it needs: AI supremacy, supply chain sovereignty, energy independence, manufacturing re-onshoring, a fentanyl-controlled border narrative, and the domestic political stability to finance $2 trillion annual deficits without a bond market revolt. The world will arrange itself around those needs — or position itself to offer alternatives. China received both Trump and Putin in the same week. That is not an accident. That is an answer.

Why it matters: A government spending $2 trillion more than it collects each year, while prosecuting a war in Iran, managing a summit architecture in Beijing, deterring action in the Taiwan Strait, and sustaining its domestic political coalition, is not facing a budgetary inconvenience. It is facing a structural arithmetic. Structural arithmetics do not announce themselves. They simply, at some point, speak. When they do, the continent that has built genuine integration — trade, energy, AI, security — will be far better positioned than three nations each managing the shock separately.

THE NEXT SIX TO TWELVE MONTHS

Iran / Hormuz. The conflict will not resolve quickly. Fertilizer disruption will extend into the 2026–2027 harvest cycle. Food insecurity in import-dependent nations in Africa, Asia, and the Middle East will deepen. Energy input costs across North American manufacturing corridors will remain elevated. Operators building logistics models on pre-conflict energy assumptions need to revise them now.

US-China. The Beijing summit produced disagreement on outcomes, not convergence. The next six months will reveal whether the trade truce hardens into durable stabilization or dissolves into the next escalation cycle. Xi’s Taiwan warning to Trump will be tested by events in the Strait, not by declarations. China’s rare earth supply management will continue as a precision instrument against US and allied semiconductor supply chains.

Taiwan–Japan. No invasion in 2026. But the permanent military readiness posture between Japan, Taiwan, and China is now an established condition — not a crisis. The accident risk rises with each new deployment. The semiconductor supply chain implications of even a partial Taiwan Strait closure are catastrophic for every technology-dependent economy on the continent.

USMCA / Sinaloa. July 1 is the decision node. Sheinbaum’s credible response to the Rocha Moya indictments before that date is the leading indicator for the review’s character. A US negotiating team that sees no credible security action will harden its USMCA posture considerably. A Mexico that demonstrates genuine institutional movement will find more room at the table. The window between now and July 1 is the most consequential diplomatic period in US-Mexico relations in a generation.

AI infrastructure buildout. The $690 billion is already deploying. Site selection decisions for data centers, mineral supply contracts, and energy agreements are being made now. North America’s window to position itself as a continental AI offer is open, but it has a closing date. Every month the three nations spend managing their bilateral Washington relationships separately is a month in which that offer goes unmade.

US debt / bond market. The bond market does not negotiate. It does not attend summits. The US debt trajectory will eventually meet a credit event — a downgrade, a failed auction, a sharp rise in borrowing costs — that changes the domestic political arithmetic for every commitment Washington is currently making. The timing is unknowable. The direction is not.

NORTH AMERICAN INVESTMENTS — THE NUMBERS

Mexico’s effective US tariff rate: 8.28% vs. 39%+ for Chinese goods. Monterrey industrial vacancy below 3.5% — effectively full. Querétaro data center land values up 340% since 2024. Northern Mexico industrial rents up 39% in 12 months. USMCA uncertainty is creating pause in long-lead investment decisions; deferral cost accumulates weekly toward July 1.

FROM THE ARCHIVE

If you are new to The North American — 77, these are the pieces that built the frame for everything we are watching unfold today. Read them in sequence — each one named a pressure point before it became the front page.

May 4, 2026 — The Treaty Is Reading the Fine Print · NA77 Signal, Sunday Weekly The July 2026 USMCA review was two months out. The Sinaloa indictments had just landed. Mexico had logged $40.87 billion in record FDI — a bet the country had to perform on. The World Cup was 40 days away. This issue mapped the fracture lines: the 46% effective steel tariff nobody was reporting, the trilateral review becoming bilateral, the FTO designation’s compliance implications, and the automation wave that was not waiting for any of it to resolve. Read it →

April 25, 2026 — The Continent Is Being Tested. By Itself. · NA77 Weekly Affairs, Sunday Brief The week Canada halted uranium exports — and prices spiked 41% immediately. The week two CIA agents died in Chihuahua and the sovereignty tension no one wanted to name became impossible to defer. This brief identified the continental logic beneath seven apparently separate stories: none of them were external forces acting on North America. They were the continent’s own unresolved questions about what it is. Read it →

October 24, 2025 — Mexico in the Trump Era — Is It Make or Break? · Founding Essay The founding essay that set the frame for everything that followed. Eight months before the USMCA decision node, before the Rocha Moya indictments, before the Iran war — this piece named the structural risks that are now the front page. Read it →

THE LONG VIEW- English version (Español abajo)

by Eduardo Joffroy G.

This is the moment North America has to decide whether it is a trade arrangement or a civilization-scale economic project. The AI race makes the answer urgent, because the future will reward regions that combine innovation, energy, manufacturing, and trust. The U.S. can lead, but it cannot build the next system alone. Mexico and Canada can matter more than ever if they stop acting like adjacent markets and start acting like strategic partners.

The U.S. has scale, capital, and AI leadership. Canada brings resource depth, financial stability, and institutional credibility. Mexico offers manufacturing capacity, demographic energy, and geographic proximity to the world’s largest consumer market. Together, the three countries already possess the ingredients of a continental advantage that no external rival can easily replicate. The weakness is that these advantages still operate too separately — with too little coordination in border policy, permitting, infrastructure, and technology strategy.

The tensions between the three nations have rarely been sharper — but tension and cooperation are not mutually exclusive. This is precisely where the Ambos framework moves from cultural concept to strategic imperative: the understanding that two realities can exist simultaneously without canceling each other. Mexico and the United States can address cartel penetration of governance — real, documented, and now a matter of federal record — while simultaneously advancing the trade architecture, energy agreements, and migration frameworks that serve both nations’ long-term interests. These are not sequential problems requiring sequential solutions. They are parallel tracks, and the continent cannot afford to let the urgent crowd out the essential.

With Canada, something genuinely unprecedented has appeared: a political coldness between Washington and Ottawa that two nations bound by a century of shared security, shared infrastructure, and shared values have never before allowed themselves. Trump’s tariff threats and Canada’s retaliations have moved the relationship into uncharted territory. Both nations know, beneath the current noise, that they are lifelong partners — and that the real test of a durable alliance is exactly this: the capacity to separate momentary political disagreements from structural long-term interest, and to hold both in view at once. That discipline is not optional. It is what separates an alliance that endures from one that fractures precisely when it is needed most.

The USMCA review could become a political contest instead of a renewal of confidence. Mexico could lose momentum if insecurity and corruption scare away the investment wave it is trying to capture. North America could remain fragmented while China scales industrial policy and AI deployment faster than any single regional response. Or the three countries could choose differently — and turn this moment of global fracture into the founding argument for genuine continental integration.

The continent that understands this first — and builds accordingly — will not merely survive the fracture. It will define what comes next.

THE LONG VIEW- Versión Español

por Eduardo Joffroy G.

Este es el momento en que Norteamérica debe decidir si solo es un acuerdo comercial o un proyecto económico de escala civilizatoria. La carrera de la inteligencia artificial vuelve esa decisión urgente, porque el futuro premiará a las regiones que integren innovación, energía, manufactura y confianza. Estados Unidos puede liderar, pero no puede construir el próximo sistema solo. México y Canadá pueden importar más que nunca si dejan de comportarse como mercados vecinos y empiezan a actuar como socios estratégicos.

Estados Unidos tiene escala, capital y liderazgo en IA. Canadá aporta profundidad en recursos, estabilidad financiera y credibilidad institucional. México ofrece capacidad manufacturera, energía demográfica y proximidad geográfica al mercado de consumo más grande del mundo. Juntos, los tres países ya poseen los ingredientes de una ventaja continental que ningún rival externo puede replicar fácilmente. La debilidad está en que estas ventajas aún operan demasiado separadas — con muy poca coordinación en política fronteriza, permisos, infraestructura y estrategia tecnológica.

Las tensiones entre las tres naciones raramente habían sido tan agudas — pero tensión y cooperación no son mutuamente excluyentes. Es precisamente aquí donde el marco Ambos deja de ser concepto cultural para convertirse en imperativo estratégico: la comprensión de que dos realidades pueden coexistir sin anularse. México y Estados Unidos pueden atender la penetración cartelesca de la gobernanza — real, documentada y ya constante en el registro federal — mientras simultáneamente hacen avanzar la arquitectura comercial, los acuerdos energéticos y los marcos migratorios que sirven los intereses de largo plazo de ambas naciones. Estos no son problemas secuenciales que exigen soluciones secuenciales. Son carriles paralelos — y el continente no puede permitirse que lo urgente desplace a lo esencial.

Con Canadá ha emergido algo genuinamente sin precedente: una frialdad política entre Washington y Ottawa que dos naciones unidas por un siglo de seguridad compartida, infraestructura compartida y valores compartidos nunca antes se habían permitido. Las amenazas arancelarias de Trump y las represalias canadienses han llevado la relación a un territorio que ninguno de los dos había cartografiado. Ambas naciones saben, debajo del ruido actual, que son socios de toda la vida — y que la prueba real de una alianza duradera es exactamente esta: la capacidad de separar los desacuerdos políticos momentáneos del interés estructural de largo plazo, y de mantener ambos en perspectiva al mismo tiempo. Esa disciplina no es opcional. Es lo que separa una alianza que perdura de una que se fractura precisamente cuando más se la necesita.

La revisión del T-MEC podría convertirse en una disputa política en lugar de una renovación de confianza. México podría perder impulso si la inseguridad y la corrupción ahuyentan la ola de inversión que intenta capturar. Norteamérica podría seguir fragmentada mientras China escala su política industrial y el despliegue de IA más rápido que cualquier respuesta regional individual. O los tres países podrían elegir diferente — y convertir este momento de fractura global en el argumento fundacional de una integración continental genuina.

El continente que entienda esto primero — y construya en consecuencia — no solo sobrevivirá la fractura. Definirá lo que viene después.

SOURCES

The North American — 77 · Sunday Morning Affairs · www.thenorthamerican.com · ONE FUTURE. THREE NATIONS. © 2026

Eduardo Joffroy · eduardo@joffroy.com · linktr.ee/ejoffroy