The Treaty Is Reading the Fine Print

The July 2026 USMCA review is two months out. The 46% tariff reality no one is reporting, the Rocha indictment, $40.87B in FDI, and the question North America cannot avoid.

The July 2026 USMCA review is two months out. The three-nation framework holding North America together is being stress-tested by tariffs, bilateral sidelines, federal indictments of Mexican officials for cartel collaboration, and oil near $105. This week, the continent showed its fracture lines — and the forces that will define the next decade.

From the Editor

“The continent is not breaking apart. But it is sorting itself. The question is whether the builders are faster than the breakers. This week’s Signal suggests they might be — barely.”

The Signal

Trade Policy · AmCham Mexico · SeaVantage · The Economist · The Bridge

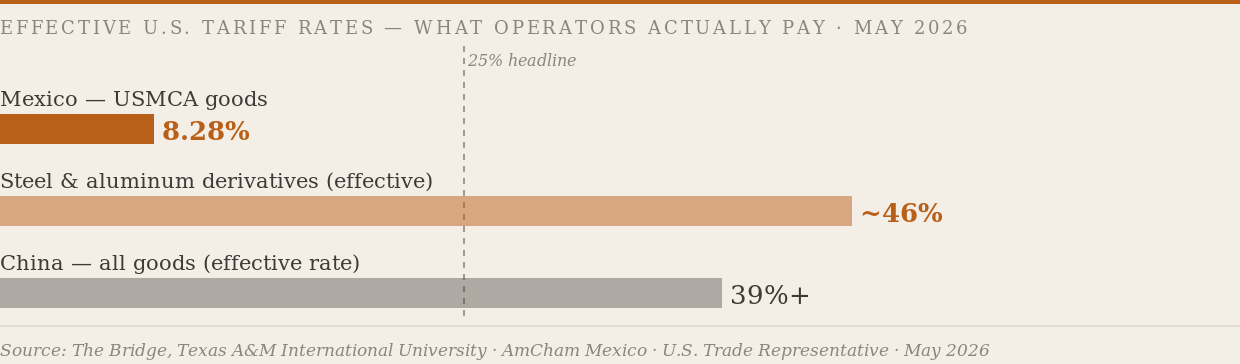

The 46% Nobody Is Talking About

The announced reduction from 50% to 25% on Section 232 derivative tariffs generated predictable headlines. The operative number is not 25. When the five new rate tiers are weighted against the actual distribution of US-Mexico and US-Canada bilateral metals trade, the effective tariff lands at roughly 46%. The gap between what Washington announces and what operators pay has become the defining feature of this trade environment.

“Weighting the five new rate tiers by where bilateral US-Mexico and US-Canada metals trade actually sits, the effective tariff lands at roughly 46%, not 25%.”

— Dr. Daniel Covarrubias · The Bridge · Texas A&M International University · May 1, 2026

The auto sector received the cleanest outcome — a separate Section 232 action adopted USMCA’s content-tracing logic, a genuine structural win for North American manufacturing. The metals proclamation did not follow that logic. The gap is real and priced into every procurement decision in the corridor right now.

The broader picture favors Mexico. AmCham Mexico shows Mexico operating at an effective U.S. tariff rate of 8.28% — versus over 39% for China. On $976 billion in annual bilateral trade, that differential is the strongest structural argument for the nearshoring thesis. The Economist calls the July 2026 USMCA review the highest-stakes trade negotiation since NAFTA. The advantage is real. It does not survive a failed review.

SeaVantage’s vessel tracking shows port congestion building at U.S. West Coast and Gulf entry points — importers front-loading ahead of anticipated rate escalations. The surge is compressing cross-border capacity on the Laredo corridor. It will normalize. Price the volatility into Q3 logistics contracts now.

Canada imposed C$15.6 billion in retaliatory tariffs on U.S. steel and aluminum. Mexico has not. Two nations, same window, different instruments — and that asymmetry will define the starting position of every conversation inside the July review.

~46%

Effective rate on USMCA steel/aluminum derivatives — vs. 25% headline · Source: The Bridge

8.28%

Mexico’s effective U.S. tariff rate — vs. 39%+ for China · Source: AmCham Mexico

$976B

Annual US-Mexico bilateral trade · Source: AmCham Mexico

Why it matters: Operators cannot price on headlines. The effective rate is the business reality. Mexico’s tariff advantage over China is structural — and conditional on the July review. Build your scenario plans around what it delivers, not what it promises. And subscribe to The Bridge. The corridor needs more analysis that shows the math.

Geopolitics · Perplexity / Multiple Sources

USMCA Was Three Nations. The Review Is Two.

The July 2026 USMCA review has shifted from a routine institutional exercise into something more consequential: high-stakes bilateral negotiations between the U.S. and Mexico, with Canada notably sidelined from the initial talks. If trilateral consensus fails, the architecture defaults to annual reviews — a slow erosion of the rule-based predictability that made the corridor attractive to capital in the first place.

U.S. indictments of Sinaloa’s governor and former officials for cartel collaboration have introduced new friction into an already compressed diplomatic timeline. Trade talks and security politics are now running on the same track. Trump’s broader geopolitical posture — Venezuela intervention fallout, BRICS military exercises in the hemisphere — is testing U.S.-Canada alliance cohesion at the worst possible moment for trilateral unity.

The IMF has trimmed 2026 global growth to approximately 3.1%. Oil near $105 a barrel embeds a persistent logistics cost premium across the continental economy. U.S. retail gasoline averaging $4.23/gallon generates political pressure that could destabilize the review timeline unpredictably.

Why it matters: A bilateral USMCA is not USMCA. The three-nation framework is the architecture’s value. When Canada is sidelined, every investment thesis built on continental integration has to be recalibrated. The question for operators: are you building for the continent that exists, or the one the agreement promised?

Geopolitics & Rule of Law · U.S. Department of Justice · NA77 Editorial

The Indictments Are Not the Story. The System They Describe Is.

When the U.S. Department of Justice named Sinaloa Governor Rubén Rocha Moya in a federal indictment for cartel collaboration, Washington did not merely accuse a state official of corruption. It named a Morena governor — a member of the governing coalition of the Mexican state. The cartels in Mexico are not a criminal layer sitting beneath governance. In too many territories, they are governance: through municipal contracts, electoral support, judicial intimidation, and the quiet collaboration of officials who have no safe alternative. When the U.S. names a sitting governor, it is not pointing at one corrupt individual. It is pointing at a system national in scope.

The Trump administration’s FTO terrorist designation of major Mexican cartel networks changes the legal architecture of U.S.-Mexico security cooperation entirely. U.S. law now authorizes financial, intelligence, and potentially kinetic tools previously unavailable. Mexico’s political class understands this. Some are afraid. They should be.

The Morena Question

Morena was built as a movement of national dignity — against the elite networks that governed Mexico through institutional corruption, and against foreign interference in Mexican sovereignty. That identity now faces its most serious internal contradiction: if the governing coalition contains officials whose collaboration with designated terrorist organizations is a matter of U.S. federal record, the sovereignty narrative fractures from the inside. This is not an external attack on Morena. It is a mirror.

On Trump’s unpredictability: Trump’s greatest leverage over Mexico is not any specific action. It is the permanent uncertainty about what comes next — at what moment, through what mechanism, with what escalation. The indictments may be followed by sanctions, deportation operations calibrated for political embarrassment, or nothing for weeks. The uncertainty itself is the instrument. Mexico is permanently on defense — and that is exactly where Trump wants it.

What should Presidenta Sheinbaum do? The honest answer is uncomfortable: do what the institution requires, not what the coalition permits. Acknowledge the indictments with the gravity they deserve. Initiate a credible process within Morena to address cartel-affiliated officials. Signal to Washington — quietly but clearly — that Mexico is a willing partner in reducing cartel influence within the governing apparatus. The political cost of cooperation is real. The cost of defiance, when the adversary holds a terrorist designation and controls the largest economy on your northern border, is potentially catastrophic.

The indictment timeline and the electoral calendar are now on the same track. With state elections approaching and the 2027 legislative cycle ahead, every new accusation narrows Morena’s political space. The party that came to power promising to end systemic corruption is now defending officials accused of cartel collaboration in U.S. federal court.

For every CEO in Stuttgart, Seoul, Chicago, Montreal, Monterrey or Detroit, making capital allocation decisions: the question is no longer whether Mexico has a cartel problem. It is whether Mexico’s government has the will to separate itself from that problem before the bilateral relationship deteriorates to the point where the investment thesis is at risk.

What This Means for Operators — Garrigues Mexico

Garrigues Mexico’s compliance brief on the FTO designation is required reading for any company operating in the corridor. Under U.S. law, organizations providing “material support” to FTO-designated entities face criminal and civil liability — with U.S. jurisdiction explicitly expanded to cover acts occurring outside U.S. territory. Action items: enhanced due diligence on all Mexican counterparties and logistics providers; updated AML/CTF protocols calibrated for high-risk corridors; supply chain resilience standards accounting for cartel territorial control; and a documentation framework establishing what your organization knew, when, and what steps it took. The window of plausible deniability is closed.

Why it matters: The FTO designations are not rhetorical gestures. They are a legal architecture change that gives the U.S. government tools it did not have before — and that Mexico’s political class cannot ignore. The USMCA review, the FDI thesis, the nearshoring corridor — all of it sits downstream of one question: can Mexico’s government credibly separate itself from cartel influence before Trump decides the answer is no?

Investment · Invest MTY · Expeditors Horizon · Perplexity

$40.87 Billion. In a Year of Tariff Volatility.

Mexico logged record foreign direct investment of $40.87 billion in 2025. Not a number that fits the hesitation narrative. It is long-duration capital from automotive assemblers, advanced manufacturers, and semiconductor-adjacent suppliers — betting on Mexican geography within the USMCA corridor regardless of Washington’s tariff posture in any given quarter.

$40.87B

Mexico FDI in 2025 — a record, driven by automotive and advanced manufacturing

Editorial Perspective

A record FDI number is a bet — not a verdict. Mexico must resist the temptation to read $40.87 billion as confirmation. It is an invitation, conditional on delivery. The foreign capital now planted in Mexican soil will either grow into a generational transformation or quietly exit to the next geography that offers what Mexico promises but cannot yet guarantee.

The honest ledger: supply chain infrastructure outside Northern and Central Mexico’s industrial triangle remains underdeveloped for the volume now being demanded. The legal system has not kept pace with the investment thesis being sold to boardrooms around the world. Energy — electricity, water, gas — is a persistent constraint, made more acute by a state-owned CFE and Pemex that are not delivering at the scale the moment requires. Security remains a negotiated reality in too many corridors. And the domestic economy is not keeping pace: internal consumption is weak, a disproportionate share of the population remains unbanked, and GDP per capita is far from the threshold a prosperous country requires.

Mexico’s economy is heavily sustained by FDI — which makes every Morena political decision a make-or-break moment for the nation’s economic trajectory. Pemex is in losses and deep debt. The moment FDI loses confidence, there is no domestic engine large enough to fill the gap. Mexico needs urgent supply chain infrastructure and energy investment to maintain its attractiveness — not in five years. Now.

On the ground, the corridors are performing. Invest MTY shows Monterrey’s industrial vacancy below 3.5% — effectively full. More than 100 Japanese companies now operate in the metro area. France’s cumulative FDI in the corridor has surpassed $218 million since 2006. The capital is there. The question is whether the infrastructure and institutions can keep pace with it.

On logistics, Expeditors’ Gervasio Verdaguer identifies the four port corridors that will carry the nearshoring volume: Manzanillo (Latin America’s largest container port), Lázaro Cárdenas (Pacific deep-water industrial gateway), Altamira (Gulf, energy and automotive supply chains), and Veracruz (the historic Gulf gateway being modernized for container growth). Mexico’s 13 free trade agreements covering 50 countries are an underused competitive advantage. The multimodal infrastructure is improving. It is not yet where it needs to be for the volume projected over the next decade.

Why it matters: Capital is patient for a reason — it expects structural return. The investors building in Saltillo and Querétaro are not doing Mexico a favor. They are making a calculated bet that Mexico will close the gap between its geographic advantage and its institutional capacity. If that gap closes, Mexico becomes something historically rare: a developing country that seized its inflection point. If it doesn’t, the window will have closed without a country on the other side of it.

Energy · Perplexity

The Bridger Approval and What It Signals

Trump has approved the Bridger Pipeline Expansion — 550,000 barrels per day of Canadian crude moving southward, reviving the debate Keystone XL made famous and never resolved. Cross-border energy infrastructure is back as a strategic instrument, not just an operational asset.

At $105 oil and $4.23 retail gasoline, North America’s energy interdependence is visible in every fuel receipt on the continent. The corridor is not energy-independent. It is energy-integrated — which means shocks in one node travel fast. The Bridger approval signals that the U.S. still needs Canadian supply, regardless of its tariff posture. That asymmetry matters.

Why it matters: Energy flows are the continent’s circulatory system. Political noise around tariffs operates on a shorter cycle than a pipeline. Build for the pipeline timeline.

Supply Chain & Technology · Supply Chain Brain · Cargado · Manifest 2027

The Machines Are Not Waiting for the Review

Supply Chain Brain’s 2026 industry survey found that 70% of North American shippers expect 5–15% growth over the next two years — in a tariff environment most analysts assumed would suppress confidence. The more consequential finding: agentic AI is no longer a pilot program in logistics. It is embedded into the operational core — demand sensing, carrier selection, exception management, last-mile rerouting.

On the cross-border corridor, Cargado’s freight data shows Laredo volumes tightening — a direct consequence of the front-loading surge SeaVantage is tracking at the ports. Operators relying on Laredo for just-in-time replenishment should be watching this closely. The tightening is not fully priced into forward planning cycles.

The physical infrastructure of North American commerce is being quietly rewired by capital and code. This week’s moves: Home Depot acquired Simpl Automation to accelerate warehouse automation across its distribution network. Siemens and KION are partnering on AI-powered digital twins for warehouse operations — compressing the decision cycle for capital-intensive logistics infrastructure. Kodiak AI and Bosch have begun hardware deliveries for autonomous freight trucks, stepping from pilot to commercial-scale deployment on the Laredo-to-Chicago corridor. Rivian is repurposing old EV batteries to power its Illinois factory — the largest repurposed battery storage system for a U.S. automaker, in partnership with Redwood Materials.

Investor signal: Sereact raised a $110M Series B for AI warehouse robotics. Eclipse closed a $1B fund focused on physical industries. Avery Dennison put $75M into Wiliot’s IoT supply chain sensors. Capital is flowing toward the physical layer of North American commerce — not away from it.

Why it matters: The automation wave is not a future threat. It is a present competitive differentiator. Corridor operators who deploy fastest will set the cost floor. Everyone else will defend against it.

The Intelligence Frontier

Space · AI · Technology · SpaceX / NVIDIA / Anthropic / xAI · NA77 Intelligence Watch

The Continent’s Other Build — Chips, Models, and Rockets

While the policy debate centers on tariffs and treaty timelines, a parallel set of organizations is building the infrastructure of the next economy — on this continent, right now.

SpaceX · Starbase, Boca Chica, Texas — Starbase sits on the Rio Grande, in Cameron County, at the US-Mexico border. The V3 vehicle — Booster 19, Ship 39, Raptor 3 engines — stands 408 feet tall, designed to carry over 100 tons to low Earth orbit. Flight 12, the first V3 test, is targeting mid-May. The continent’s most ambitious manufacturing program is being built at the border, not in spite of it. The economic spillover into South Texas and Tamaulipas from this concentration of engineering talent and supply chain activity is a story North America has barely begun to tell.

NVIDIA · Vera Rubin Platform — Six new chips delivering a 3-to-4x improvement in compute density over Blackwell, reducing AI inference token costs by roughly 90%. NVIDIA projects the total AI infrastructure market at $1 trillion by 2027. The practical meaning for corridor operators: the compute floor is collapsing. What required a data center budget last year will run on a workstation budget next year. Organizations that understand this will compress decision cycles in ways that competitors will struggle to catch.

Anthropic · Claude — Claude Opus 4.7 is now generally available with improvements in complex long-horizon tasks. Claude Design launched for visuals, prototypes, and one-pagers, with creative connectors live for Blender, Autodesk Fusion, Adobe Creative Cloud, and Ableton. Harvard’s Faculty of Arts and Sciences moves from ChatGPT Edu to Claude for institutional AI access. The NA77 Signal is human led & Claude built — and the compression of editorial workflows that used to require teams is available to every operator and organization in the corridor willing to use it.

SpaceX / xAI · Structural Consolidation — xAI has been merged into SpaceX, combining orbital launch capability with large-scale AI inference, targeting an IPO in June 2026 at a reported valuation of $1.75 trillion. In federal court this week, testimony confirmed that xAI’s Grok was trained on OpenAI models — a disclosure with significant implications for how the AI competitive landscape is understood. The consolidation of space and AI under one North American private entity has no clear precedent. Watch it with clear eyes, whatever one thinks of the individuals involved.

Why it matters: The treaty, the tariffs, the security crisis — these are the operating conditions of today’s corridor. The compute platforms and launch infrastructure being built right now are the operating conditions of tomorrow’s. North American leaders who engage only with today’s policy debate will find themselves governing a continent they no longer recognize.

World Cup 2026 — Continental Countdown

FIFA World Cup 2026 · Mexico / United States / Canada · NA77 Readiness Watch

40 Days Out. Is North America Behaving Like One Continent?

FIFA WORLD CUP 2026 — NORTH AMERICA · JUNE 11 – JULY 19CANADAToronto · VancouverUNITED STATES11 cities · MetLife Final · July 19MEXICOAzteca · BBVA · Akron104 matches · 48 teams · 16 host cities · 40,000 jobs · $5B+ projected economic activity across North America

On June 11, the world arrives in North America. Mexico opens at Estadio Azteca — Mexico versus South Africa — in the first World Cup in history co-hosted by three nations. The final is July 19 at MetLife Stadium. Between those two dates, three nations, 48 teams, and a global television audience will form their opinion of this continent’s capacity to function as a shared enterprise.

The readiness picture is mixed. At least three host cities received formal FIFA notices flagging incomplete transportation or fan zone infrastructure. In Kansas City, light rail capacity expansions remain only partially complete. The U.S. Department of Transportation has allocated $220 million for transit corridor improvements; FEMA is distributing $625 million in security grants to host city committees. These are significant commitments. Whether they translate into seamless cross-border execution is a different question.

Mexico’s three host cities tell different stories. Mexico City opens the tournament at the Estadio Azteca with 100,000 security personnel deployed — though a shooting at Teotihuacán in April accelerated security mobilizations with less than 60 days remaining, a reminder that security commitments and security reality in Mexico are not always the same variable. Guadalajara will manage. Monterrey is attempting something larger: Governor Samuel García’s FIFA Corridor links the airport, Estadio BBVA, and Parque Fundidora through redesigned mobility — 2,200 eco-friendly buses, 400 new TransMetros, and the centerpiece Metro Lines 4 and 6, expanding from 38 to over 80 kilometers of rail. As of late 2025, both lines were approximately 60% complete. Whether the system opens at full capacity, partial capacity, or ceremonially on June 11 will tell us a great deal about the gap between Mexico’s infrastructure ambition and its delivery capacity.

The NA77 Question

If Monterrey delivers — if the monorail runs, the FIFA Corridor flows, and the city handles the crowd with the sophistication of a genuinely world-class industrial metropolis — it will be one of the most meaningful infrastructure legacies any Mexican city has produced in a generation. The window to use a once-in-a-generation global event as a permanent transformation catalyst is narrow, and it only opens once.

The structural risk is not the stadiums or the hotels. It is the seams between systems. A fan traveling from Toronto to Monterrey to New York for three group stage matches crosses two international borders, three immigration regimes, and multiple transit systems not designed to work together. The three nations have coordination structures. What they do not clearly have is a shared operational command that treats the 40-day tournament as a single continental logistical event.

The NA77 Argument

The more unified the security and operational response across the three nations, the safer every fan in every city will be. A threat that originates in one country and travels to another — a coordinated attack, a public health emergency, a massive crowd incident — requires a response architecture that does not stop at a border. If the three nations cannot build that architecture for 40 days of football, the question of whether they can build it for the harder challenges ahead becomes very difficult to answer optimistically.

North America has spent thirty years proving it can integrate around trade. The 2026 World Cup is the first test of whether it can integrate operationally — on security, mobility, and public safety. Whether the three governments look at July 20 and ask “what did we learn, and how do we build on it?” is the question that will determine whether 2026 is a moment or a milestone.

Why it matters: North America is good at trade. The 2026 World Cup is a 40-day test of whether it can go further — from commercial partners to genuine operational collaborators. A successful tournament, coordinated across borders with visible fluency, would do more for the narrative of North American integration than any trade agreement in thirty years. The continent will learn something about itself. The question is whether its leaders are paying attention.

On the Radar

July 2026

USMCA Review Deadline. The pivot point for North American trade architecture. Trilateral consensus or bilateral fragmentation. The most consequential policy moment for the continent this decade.

Sept 27–29

North Capital Forum 2026 — Mexico City. Led by Enrique Perret, CEO of the US-Mexico Foundation, NCF 2026 convenes CEOs, government leaders, legislators, and innovators for three days on the future of North America — trade, energy, technology, and supply chains. This is where the continent’s builders gather and where the conversations that shape the corridor actually happen. We are proud to support Enrique’s work and encourage every reader building across the border to put September 27–29 on the calendar.

Feb 8–10, 2027

Manifest 2027 — Las Vegas, Nevada. The continent’s defining logistics and supply chain innovation conference returns to The Venetian, presented by DHL. Courtney Muller, President of Manifest, has built what is now the essential annual gathering for freight technology, capital, and operational intelligence in North American commerce — 7,200+ attendees in 2026. If you are building in the corridor, this is where the intelligence concentrates and where the relationships that shape the next year get made. Put February 8–10 on the calendar now.

Ongoing

Semiconductor supply chain resilience. Supply Chain Brain’s 2026 intelligence series focuses on structuring for the next shortage cycle — not just managing the current one. The continental bet on U.S. and Mexican semiconductor-adjacent manufacturing is the long play underneath the tariff noise.

The Long View

By Eduardo Joffroy G · The North American — 77

The Game Needs a Fair Referee. North America Must Decide Whose Side It’s On.

Business and trade are energy. They are trust in motion. When you stop them — even for a reason that seems good in the room — you do not pause an economy. You drain it.

North America has three players in this game. The question — this week and every week this Signal publishes — is whether each of them is bringing their A game. From the private sector and from the public sector. From the boardroom and from the government. Because when a referee stops calling the game fairly, when rules shift mid-play, when one team receives preference — the whole game suffers. The players adapt around it. But the cost compounds.

The United States is not waiting. Its private sector is moving with the urgency the moment demands. On the Rio Grande at Boca Chica, Texas, SpaceX is building Starship — the most ambitious spacecraft in human history — steps from Mexican territory. In Arizona, TSMC and Intel are building the semiconductor cluster that will supply the AI economy for the next decade. The capital is flowing. The compute is being built. The infrastructure of the next era is rising at the edges of the North American continent, looking south and north for partners who are ready to receive it.

Canada has the natural assets to be indispensable. Vast clean hydroelectric power that could feed the energy-hungry data centers the AI economy demands. Critical minerals essential for semiconductor supply chains. Institutional capacity and rule of law that Mexico cannot match at present. What Canada needs right now is a clearer vision of what it is building — and for whom. Its tariff retaliation posture is tactically understandable. Strategically, it risks the continental architecture that benefits Canada most.

Mexico’s situation is the hardest to write honestly — because the honest assessment is uncomfortable. Mexico’s private sector is performing. The $40.87 billion in FDI, the Ternium steel mill in Pesquería, the Japanese companies filling Monterrey’s industrial parks to below 3.5% vacancy — this is Mexico’s private sector bringing its A game, against real odds, in a difficult environment. The problem is not the private sector. The problem is the public sector that is not showing up to the same game.

SpaceX is building Starship minutes from Mexican territory. TSMC and Intel are constructing the semiconductor future in Arizona — close enough that Sonora should be a logical manufacturing extension. The world is not happening far away from Mexico. It is happening on Mexico’s doorstep, under Mexico’s nose, with Mexico’s geographic destiny on the table. And Mexico is watching it through a window it has not fully chosen to open. How can a country be so close geographically, and so far from its neighbors in national vision?

What Capital Is Expecting

Business is happening. Investments are being made. The bets are on North America. What capital expects in return is not complicated: legal protection that holds in court, modern infrastructure at the volume being demanded, an effective financial system, strong business clusters, proximity to market, and the overall efficiency that lets companies here compete with the world — not just with each other. That is the contract. North America must decide whether it intends to honor it — not as a declaration, but as an operating reality.

The AI Age is not primarily about deploying tools. It is about understanding the paradigm shift — and moving to capture the opportunities the shift creates before someone else does. The world is automating. It is competing at a speed and scale that requires reliable energy, manufacturing proximity, educated labor, and institutional agility. AI data centers alone will consume more electricity over the next decade than many nations currently produce. This is not a technology story. It is an infrastructure, energy, and governance story.

Both Mexico and Canada have more to gain from positioning themselves as first suppliers for the United States’ AI global ambitions than from any trade negotiation currently on the table. Mexico has the geographic position, the industrial corridor, the labor force — and, beneath a governing philosophy that looks inward, the solar and wind potential to power the data centers that will define the next economy. Canada has the hydroelectric power, the critical minerals, and the institutional credibility. The opportunity is there for both nations. It does not wait for political cycles to resolve themselves.

Mexico’s public sector is the variable — and it is the one that Mexico controls. An energy policy that opens CFE to private and international investment, rather than defending a Pemex bleeding losses and deep debt, would change the investment equation overnight. A governing coalition that stops defending cartel-affiliated officials and starts building digital infrastructure and AI readiness could accelerate Mexico’s position in a single legislative cycle. The private sector is ready. The capital is ready. Geography has already placed Mexico next to the most powerful economy on earth. What is missing is not opportunity. It is the decision to honor it.

North America must act as North America. Not three nations managing each other’s expectations — one continental economy choosing to compete with the world. The players are ready. The capital is in. The World Cup is coming. All that is missing is the decision to let the game run.

— Eduardo Joffroy G · Founder, The North American — 77 · May 3, 2026

ONE FUTURE. THREE NATIONS.

This week’s Signal is heavier than most — and deliberately so. The continent is carrying a full load: a trade treaty being stress-tested, a governing coalition facing federal indictments, record investment in a country being asked to prove it deserves it, a World Cup 40 days out that will test whether three nations can actually behave as one, and a technological infrastructure being built at the border and in the data centers that will define the corridor for decades. North America is not a simple story. It never was. The work of this publication is to tell it honestly — and to keep finding the people who are building it right.

NA77 Signal is curated weekly intelligence on what’s moving North America — trade, energy, capital, technology, and the people building across the corridor.

Published every Sunday. Written by the NA77 Team from Tucson, Monterrey, and the road between them.